Liquor store financing is vital to owning a wine and spirits small business. In many states, liquor store owners are compelled by law to pay for merchandise within thirty days. In some states like Florida, that payment horizon is ten days. That means if you don’t sell inventory within that time, it’s like stacking cash on your shelves. This article is all about how to manage cash flow in a liquor store and maximize working capital. Without buying power a liquor store owner is limited to the upfront cost (within 30 days) of their cash balances.

Get Funded Now

Liquor Store Financing – Empowering Purchasing Power

Many liquor store business owners will tell you that they don’t make profits “selling”…they make their real money through “buying”. Let’s unpack that statement and find out what is meant by that. Simply put, it’s a matter of buying power and reducing the cost of goods sold. Most liquor stores will buy their products from large wholesalers. And while the price of a bottle of wine, vodka, gin or whiskey may be somewhat similar from store-to-store, the price that each store owner pays for that product on a wholesale basis can vary greatly. Buying low and selling high is the basic formula for success in any type of business.

Purchasing power is the ability to purchase products in bulk in an effort to reduce unit costs. A liquor store owner that can purchase one hundred cases of alcohol from a distributor is likely to pay a lower per-unit cost than the store owner who buys one case. In the liquor business, quantity discounts can be substantial, so having the capital to purchase in bulk is a serious competitive advantage.

The owner that buys in bulk has several options not open to his smaller counterparts. He or she may choose to sell their product at the same price as competitors and pocket the additional profit or they may choose to lower the price of the more popular brands to take more market share from competitors. In most cases, larger liquor stores will offer very low prices on the most popular items in order to attract the maximum number of customers. In some cases, that store may even lower the price so low that they break even or lose money on popular items. This is what is known as a “loss-leader”.

Liquor Store Funding – Making Money from Borrowing

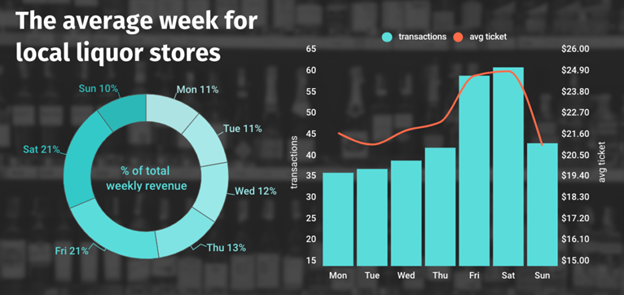

The concept may seem strange at first, but there is a retail science behind the strategy. Liquor store owners understand that most customers make multiple purchases when they visit the liquor store. According to a liquor store study conducted by Womply, the average liquor store services 43 customers per day. The average size of a purchase is approximately $24. If a store advertises a deep discount on a popular item, they have the opportunity to attract a lot more customers. When you consider that liquor store customers make multiple purchases each visit, you can begin to understand why an owner would consider discounting.

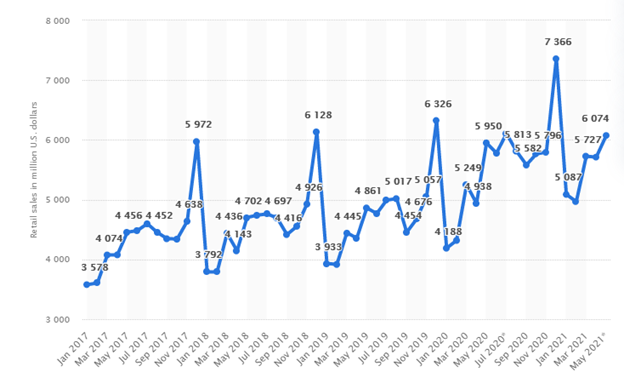

Now, let’s talk about seasonality in liquor consumption. It is widely known that liquor store sales spike during the end-of-year holiday season. Specifically, 60% of liquor store sales annual revenue occur in the last three months of the year. So, for the typical liquor store owner that wants to compete for the holiday customer rally, you need to be (financially) prepared to compete.

Taking a liquor store loan, a business line of credit, a merchant cash advance or other loan options to finance inventory purchases could mean a whopping increase in sales and profitability. In many instances, buying in bulk can mean up to 20% reduction in the price of goods sold for liquor store owners.

The busy season means that you are likely to sell your liquor store inventory 2-3 times faster than at other times of the year. If you know that you will be able to purchase at substantially lower prices and sell that inventory within three months, a liquor store financing option may make a lot of sense. Short term financing is less expensive that other types of financing so, if you are looking to compete with larger retail liquor stores this holiday season, you may wish to consider inventory financing to make the most of the holiday sales season.

Loan Amounts and Repayment Should Drive Your Business Financing Choices

Understanding how much you should borrow to finance inventory purchases should be measured by looking at past history for the months of October, November and December, and balanced against the business need. Once you have an idea of what products you will sell in what amounts you can then start to match those numbers against various loan programs and funding options. If you have a new store or a new location for your store, you may want to consult some of your distributors to gain some insight on potential sales volumes you can expect from the new location or new liquor store. Keep in mind startup liquor stores may be harder to finance unless you own the real estate.

There is no formal designation for liquor store business loans, but borrowers are sure to find many suitable options like small business loans, traditional bank loans, term loans or even an SBA lender program. Keep in mind, an SBA loan may take 6-8 weeks or more to process. You may wish to check the Small Business Administration website for complete details. The SBA will also require borrowers to submit a business plan. The most popular SBA loans are SBA 7 loans. The SBA 7 loan is formally called the SBA 7(a) loan and does not require collateral.

Many liquor stores have very high percentage of credit card sales which makes them ideally suited for a merchant cash advance, but these business funding options can be expensive compared to interest rates from traditional lenders. One of the benefits of an MCA loan is that it does not require a credit score check, but you may be required to submit a tax return. Also, you will likely to submit copies of your bank account statement for the past two years. Small business owners should be careful to check the terms of their MCA loan carefully.

While liquor stores are still seen as high-risk businesses, they are also seen as recession-proof and therefore a popular choice for alternative lenders.